From Climate Change to Asset Prices

by Riccardo Rebonato, Professor of Finance, EDHEC Business School and Scientific Director, EDHEC-Risk Climate Impact Institute

The last ten or so years have seen a sea change in the degree of engagement of the financial and investment communities with climate change. There have been innovative ideas to finance the (massive) investment required to build renewable sources of energy to scale or establish carbon sequestration and negative-emission technologies. There has also been a strong commitment by many asset managers to disinvest from carbon-emitting sectors, and to invest in green industries, thereby shifting, it is hoped, the relative cost of capital. Some major sovereign investment funds have taken resolute steps in this direction as well. And, with more and more insistence, investors have begun to ask the existential question of whether it is indeed possible to do well while doing good.

All of these steps are encouraging. The focus, however, has so far mainly shifted from finance to the abatement of climate change. Another, equally important, dimension should be considered: what will the impact be of climate change, and of the seriousness of our abatement effort, on asset prices? How will investors fare under different scenarios of climate change abatement and climate outcomes? There is more to answering this question than looking at `winners and losers’ in different sectors under different climate scenarios, assessing the value of stranded assets, or gauging the sectoral impact of adaptation. It is not just the climate outcomes, but also our actions in abating climate change – or lack thereof – that will have a profound effect on asset returns. We are only just beginning to acquire the analytical tools to answer these questions. The implications for investors are going to be major, but they are still poorly understood.

How will climate outcomes and abatement efforts affect returns on capital? First of all, there is what I call a size-of-the-pie effect. For fixed proportions of the economy’s output going to labour and capital (not an ‘innocuous’ assumption, by the way), what the providers of capital will receive is a fixed fraction of what the economy will produce. The gross product (the size of the pie to be divided) will in turn be affected by how much damage climate change will inflict, and by how much we will decide to invest in mitigating this damage. This size-of-the-pie effect is likely to be the first-order contributor to asset returns. It is still imperfectly understood.

The second effect on asset returns has to do with the massive redirection of resources required to move the ‘climate needle.’ Just a few figures can give a feel for the magnitude of a meaningful abatement effort. Just before the latest UK elections, the three main parties pledged that 20, 30 and 60 million trees would be planted to capture CO2 emissions. Whenever ‘millions’ rolls off the tongue of a politician, it always sounds impressive. However, a quick back-of-the-envelope calculation shows that, if we really want forests to absorb a significant fraction of the UK’s CO2 emissions, more than 2 billion trees would have to be planted – and, in case you were wondering, that would cover more than half the surface of Wales. Or, from a different perspective, during the Second World War 2751 Liberty ships were built in the US, each requiring 7,000 tons of steel – approximately 0.1 tons per American. The UK would need ten times as much steel production per person to build the wind turbines needed to generate a meaningful fraction of domestic energy consumption.

I could go on for a long time with these jaw-dropping figures (and with my students I do). The message, however, is simple. If we carefully construct a balanced portfolio of initiatives centred on renewables, carbon-sequestration-and-capture and negative emission technologies it is still possible to keep the effects of climate change under control. The best science tells us that the half-hearted pace of our current abatement initiatives is worrisome, but we are not past some irreversible `tipping point’. However, whether we are going to undertake these different initiatives on the scale required to limit damage to a manageable level is far from certain.

If we carefully construct a balanced portfolio of initiatives centred on renewables, carbon-sequestration-and-capture and negative emission technologies it is still possible to keep the effects of climate change under control. The best science tells us that the half-hearted pace of our current abatement initiatives is worrisome, but we are not past some irreversible `tipping point’.

If we do, there will have to be a redirection of resources from many current forms of consumption to climate change abatement on a scale that I can only describe as a `war effort’. If we don’t, we are going to face potentially extensive (and very difficult to estimate) damage to the total economic output – not to mention the difficult-to-quantify social costs of forced migration, geographical shifts in agricultural yields, etc. Let’s assume that we collectively choose the sensible option and undertake the very-large-scale effort required. The very scale of that undertaking implies that picking sectoral winners and losers, assuming an otherwise basically unchanged investment universe, does not make a lot of sense. The cross-sectional regressions of sector returns against climate changes proxies we have seen so far may be a useful starting point, but barely scratch the surface of the problem – and can give the impression that the problem is relatively simple, and linear. Perhaps asking ourselves how world economies changed and adapted in the past during the World Wars may be a better place to start. It may not be a case of choosing between guns or butter, but it may well turn out to be a choice between wind turbines or expensive summer holidays.

It is also worthwhile remembering that the social impact of past war experiences has been pervasive and lasting. For instance, the female workforce who, for the first time in history, showed up at the factory while their husbands and brothers were on the frontline never fully went back to the kitchen and the laundry room. This temporary wartime ‘stopgap’ ended up having transformational effects on Western society, both from a social and economic perspective. Whenever the productive resources of a society have to be significantly rechannelled, major social transformation are the norm, not the exception.

Looking at the scale of the required abatement investments, we can then ask ourselves, for instance, what the societal impact will be of producing the million tons of steel needed for the wind turbines. It is a received fact of economic growth theory that, as societies become richer, the fraction of services rendered outstrips the demand for physical goods: rich people want better and more frequent restaurant meals, not an extra refrigerator. Could the need for labour-intensive renewable sources of energy (such as wind turbines) upend this trend? If this were to happen, could this shift back towards manufacturing alter the current capital/labour share of the economy’s output? Is the 30/70 split a law of nature or a historical accident? And, if manufacturing were to see a partial renaissance, would the production of the turbines and solar panels be outsourced, or satisfied domestically?

Finding our bearings in this extremely complex landscape is daunting. How can we make the connection from the ‘size of the pie’ and the redirection of resources on the one hand to asset prices on the other? The task seems forbidding, but, luckily, a suite of analytical tools have been honed in the last decade that can provide a sensible starting point for tackling these questions in a logically coherent manner. I am referring here to the so-called Integrated Assessment Models (IAMs), of which Prof Nordhaus’ DICE model is probably the best known.[1] These models attempt to provide an integrated (hence the name) assessment of how the physics of climate change is linked to the technology of emissions and emission reduction and both, in turn, to the economics of production for the planet as a whole, or for selected regions. By making liberal use of what physicists and economists call `reduced-form models’, these IAMs try to strike an inspired balance between being too coarse and approximate and being unmanageably complicated. They ruthlessly piggy-back on the work done by other, much larger-scale, models (such as state-of-the-art climate models) to distil the outcomes of the latter in synthetic and `policy-consumable’ higher-level model inputs. Above all, they try – admirably, I think – to avoid the most insidious temptation, i.e. to be ‘precisely wrong’.

Do these IAMs provide all the answers? Of course they don’t – nor do they try to. However, they have the great virtue of spelling out their working assumptions clearly, and of shining a spotlight on the modelling choices that really make a difference with laser-sharp precision. We may disagree with how some aspects of reality have been modelled, but good old-fashioned sensitivity analysis can then tell us whether we should worry about these shortcomings or not, and how we can fix the modelling flaws.

If one is looking for answers about the impact of abatement efforts on asset prices, these IAMs are far from being ready to plug-and-play – and for a very good reason, because they have usually been designed with a very different goal in mind: finding the socially optimal course of abatement action, and the equally optimal values for quantities such as the carbon tax. In the last decade, social optimality has unfortunately been on a collision course with political realities (read: the gilets jaunes movement, or the election of Trump in 2016). An adaptation of these models to explore outcomes away from optimality – in the human, all-too-human world we inhabit – is therefore necessary, and this is a research effort in which EDHEC is actively involved. Analysis away from the theoretically optimal, but politically unrealizable, solution is extremely important because the sensitivity of climate and economic outcomes to uncertain model parameters is magnified when one operates away from optimality.

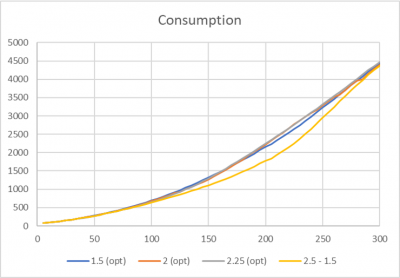

This point is both important and poorly appreciated. Many papers have been written on the sensitivity of the economic outcomes predicted by a model such as DICE on parameter uncertainty. The results have been by and large very (too?) reassuring, suggesting that, as long as we act optimally, the economic outcomes will not change by much even if model parameters assume different values. A typical example of this type of analysis is shown in Figs 1 and 2, obtained by varying over a significant range one of the most important parameters, the so-called damage exponent, i.e. the exponent that translates an increase in temperature into direct economic damage. Fig 1 shows consumption over the next three centuries projected by the DICE model for three different values of the exponent (1.5, 2 and 2.25) under two sets of assumptions: one is that, whatever the true parameters might be, we know its value and accordingly act optimally; the second is that the true parameter is 2.25 but we act as if it were 1.5. The three top tightly bunched curves in Fig 1 show that, as long as we act optimally, we will indeed roughly enjoy the same level of consumption whatever the true parameter is. The bottom yellow line, however, shows that this ceases to be the case if we cannot act optimally, i.e. if, out of ignorance or because of political constraints, we follow the 1.5 path when the true parameter is 2.25.

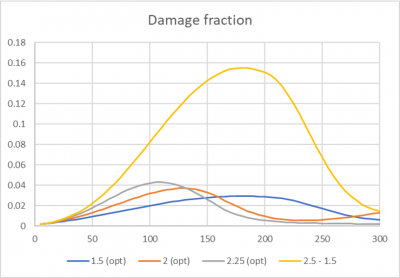

Fig 2 conveys the same message more forcefully by focussing on what the DICE model calls the ‘damage fraction’, i.e. the percentage of global output destroyed by the effects of climate change. Again, the three bottom curves show that, as long as we take optimal actions, the damage fraction never exceeds a few percentage points. However, the politically constrained social planner, who, in a 2.25 world, can only implement the policies that would be optimal in a 1.5 world, will face a damage fraction of almost one sixth of GDP.

The almost invariance of economic outcomes under very different scenarios as long as society adapts optimally may be surprising. What is happening is that an Integrated Assessment Model such as DICE is built to optimize, i.e. to search for maxima of a target function (specifically, the utility function). Mathematically the almost invariance around optimality of economic outcomes (outcomes, that is, directly related to the utility that is maximized) can be understood by recalling the first-order stationarity of a solution around an extremum. More intuitively, the DICE model moves all the physics levers at its disposal (e.g. the CO2 concentration, or the temperature analysis) to keep the economic outcomes it optimizes as close as possible to the attainable maximum.

As Figs 1 and 2 show, however, the vanishing of first-order derivatives can no longer work its magic when we move away from optimality. And, unfortunately, given the crooked timber out of which humanity has been made, we can consider sub-optimal actions as a certainty, rather than a remote possibility. This is why EDHEC has embarked on a research programme focussed on the economic and financial outcomes away from optimality. As there is but one way to be optimal, but infinitely many ways to be wrong, this approach may have less logical cogency (which of the infinitely many wrong courses of actions should we focus on?), but much greater practical relevance. The optimal paths undertaken by an enlightened politician who follows the DICE prescriptions (and only faces re-election once every eighty years) therefore assume a benchmark value, against which the least-bad practically feasible options can be assessed.

It is clear from this discussion that the link between a climate model and asset returns is far from straightforward, especially when we can no longer rely on the intellectual crutch provided by optimality. When the chosen course of abatement action is a combination of political, scientific and social compromises, all our conclusions about asset returns (both the size-of-the-pie and the cross-sectional effects) become conditional on a plausible, but far from certain, course of action being undertaken. From the modelling and analytical point of view this is far from ideal. However, Integrated Assessment Models such as DICE have one trump card (no pun intended) up their sleeve. Modern asset pricing theory is built around the concept of a stochastic discount factor: the state-dependent but security-independent quantity that transforms the future cash-flows in different states of the world into security prices. By the way they are constructed, IAMs offer the stochastic discount factor almost ‘for free’. We do not have to commit ourselves to a pricing model such as CAPM or to the Arbitrage Pricing Theory to arrive at asset prices: as long as we can specify the payoffs (something we have to do in any case), we ‘only’ need a utility function (which can be changed and made as complex as one deems necessary) for the prices of assets to fall out of a DICE-like approach almost automatically.

I don’t want to give the impression that doing so is an easy task. Nobody really knows which abatement path will be followed. And a lot of guess work has to go into assigning security-specific outcomes to different abatement paths and patterns of climate damage. However, these difficulties are common to all modelling approaches – and, given their nettlesome nature, these difficulties are usually dealt with by pretending that they do not exist. Sailing close to the shores of optimality is comforting, but not very useful. At least the framework afforded by IAMs such as DICE gives us a structured and solid way to feel our way from the questions (What will the impact be of this or that abatement choice an asset prices?) to the answers we seek.

What specific aspects could the type of analysis sketched above try to answer? Providing answers at this stage is certainly premature, but here are a few pointers to scenario-dependent questions that can be addressed with the help of Integrated Assessment Models:

- What can we expect to be distributed to equity and debt holders? And what will the equity risk premium be?

- How will Emerging Markets fare? Which geographical regions are going to be at an advantage or disadvantage?

- Will returns to capital be as generous as they have been in the last thirty years, or will labour reclaim a larger share of the total output?

- What will the sensitivities (betas) of different sectors and/or individual stock returns be to a relevant climate change factor?

- Can we obtain an estimate of the higher moments of the return distributions, from which a number of risk statistics (such as VaR estimates) can be extracted?

Arguably, few questions are going to be more relevant from the perspective of long-term investing.

References

Dietz S, Hope C, Stern N, Zenghelis D, (2007), Reflections on the Stern Review: A Robust case for Strong Action To Reduce the Risks of Climate Change, World Economics, 8 (1), 121–168

Nordhaus W D, (2007), The Challenge of Global Warming: Economic Models and Environmental Policy, Yale University, New Haven, Connecticut USA, 1-253

Nordhaus W D, Moffat A, (2017), A Survey of Global Impacts of Climate Change: Replication, Survey Methods and Statistical Analysis, NBER Working Paper 23646, http://www.nber.org/papers/w23646

Schubert K, (2019), William D Nordhaus : Integrer le Changement Climatique Dans l’Analyse Macroeconomique de Long Terme, Revue d’Economie Politique, 129 (6), 887-908

Stern Review, (2007), The Economics of Climate Change: The Stern Review, Cambridge University Press, Cambridge, UK

Footnotes:

[1] For a detailed discussion of the DICE model, and how it compares with the IAM underpinning the Stern Review, see Nordhaus (2007). Nordhaus and Moffat (2017) provide a thorough meta-analysis of the best evidence on the DICE model parameter. For a critical perspective in the same conceptual framework, see Stern Review (2007) and Dietz, Hope, Stern and Zengelis (2007). For a very clear description of how climate change science is integrated into macroeconomic analysis, see Schubert (2019).

Rubrique

About EDHEC

Operating from campuses in Lille, Nice, Paris, London and Singapore, EDHEC is one of the world’s top 15 business schools. Fully international and directly connected to the business world, EDHEC commands a strong reputation for research excellence and the ability to train entrepreneurs and managers capable of breaking new ground. EDHEC functions as a genuine laboratory of ideas and produces innovative solutions valued by businesses. The School’s teaching is inspired by its research work and a focus on “learning by doing”, all with the aim of equipping people with the skills to succeed in business.