A great success for the webinar "Introducing the Retirement Bond: The New Risk-Free Asset in Decumulation Strategies"

Written on 21 Dec 2021.

A great success for the EDHEC-Risk Institute webinar organised with over 300 professional registered to learn from top experts on the decumulation investing problem and how to solve it with the introduction of the retirement bond.

The need for retirement products to provide income security for Defined Contribution plan participants has been identified, both by regulators and the industry, as the primary goal of retirement investing. Lionel Martellini and Shahyar Safaee explained how to achieve this objective without sacrificing liquidity or flexibility.

During this one hour webinar hosted by Pensions & Investments, the world’s leading newspaper for institutional investing, our two leading experts discussed:

- The decumulation investing problem: Goal-based withdrawal and investment strategies;

- The outstanding puzzles in retirement investing: The annuity puzzle and the duration puzzle;

- The introduction of the Retirement Bond: The new risk-free asset in retirement income strategies;

- The benefits of the Retirement Bond in decumulation investment strategies.

Watch the replay

Similar to the SeLFIES (Standard-of-Living, Forward-starting, Income-only Securities) proposed by Nobel Prize Robert Merton and Arun Muralidhar, the Retirement Bond solution proposed by Lionel Martellini and Shahyar would guarantee safe income over the first 20 years of retirement.

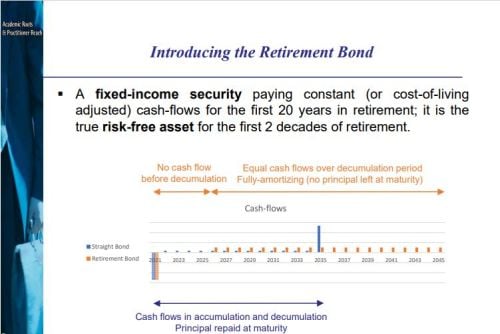

EDHEC Retirement Bond is fixed income security paying constant (or cost-of-living-adjusted) cash-flows for the first 20 years of retirement; it is the true risk-free asset for the first two decades of retirement says Lionel Martellini, Director of EDHEC-Risk Institute.

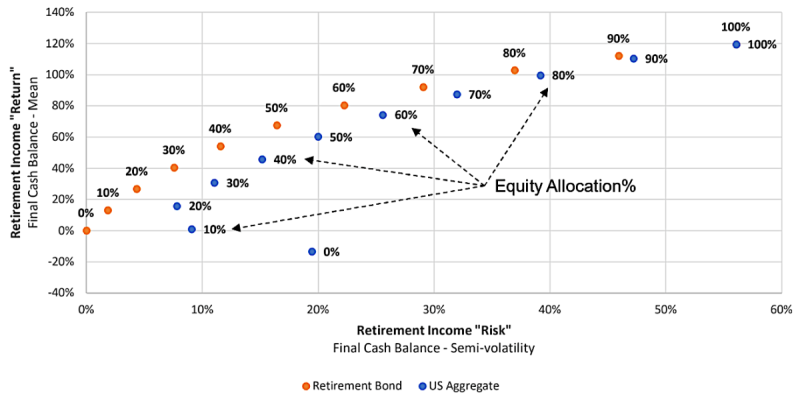

“If you’re at 30% equity allocation in retirement, that would bear the same level of retirement income risk as a 39% equity allocation, leaving an extra 9% of equity allocation availabl. Using the Retirement Bond as the fixed-Income asset enhances “risk-adjusted returns” with respect to retirement income.,” said Shahyar Safaee, Research Director and Head of Business Development at EDHEC-Risk Institute.

Note: This chart shows that using EDHEC’s Retirement Bonds for income during the first 20 years of retirement allow a higher equity allocation

and higher final cash balance than using the bonds in the US aggregate bond index – Reference Retirement Income Journal

Access insightful article "Retirement Bonds’ could increase income, lower risk: EDHEC" by Kerry Pechter, Editor of the Retirement Income Journal, which sums up well the content brought during this webinar.

You can read speaker's edito "THE DECUMULATION PROBLEM?", published in the July edition of EDHEC-Risk Institute newsletter. In a nutshell, the decumulation problem is defined as the challenge involved in efficiently turning wealth into income, which stands in direct contrast with the accumulation problem, which is instead about efficiently turning income into wealth. In individual money management, the most typical decumulation problem starts when an individual retires, ceases to receive labor income, and starts to draw down on accumulated assets to generate the level of replacement income needed to sustain the target consumption level in retirement. The problem actually extends beyond individual money management to encompass all situations where an institutional investor is tasked with the complex challenge of managing assets while facing pre-committed outflows, as would be the case for example with a mature defined benefit pension fund or an endowment. As Bill Sharpe eloquently put it, the decumulation problem is indeed a hard and nasty problem, but its importance is so overwhelming that this cannot be used as an excuse for inertia.

About EDHEC

Operating from campuses in Lille, Nice, Paris, London and Singapore, EDHEC is one of the world’s top 15 business schools. Fully international and directly connected to the business world, EDHEC commands a strong reputation for research excellence and the ability to train entrepreneurs and managers capable of breaking new ground. EDHEC functions as a genuine laboratory of ideas and produces innovative solutions valued by businesses. The School’s teaching is inspired by its research work and a focus on “learning by doing”, all with the aim of equipping people with the skills to succeed in business.