Wheat Futures Contracts: Liquidity, Spreading Opportunities, and Fundamental Factors

Industry Analysis

Wheat Futures Contracts: Liquidity, Spreading Opportunities, and Fundamental Factors

By Hilary Till

Research Associate, EDHEC-Risk Institute; and Principal, Premia Research LLC

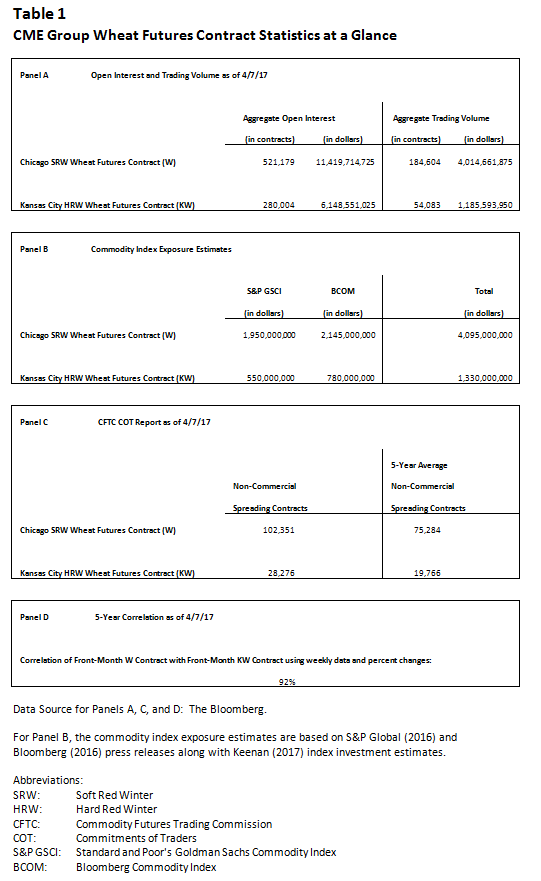

Both hedge funds and asset managers have the choice of two futures contracts at the CME Group for expressing views in the wheat markets: either via the Chicago soft red winter wheat (W) contract or the Kansas City hard red winter wheat (KW) contract. Regarding the latter contract, the CME Group acquired this contract in late 2012 when it purchased the Kansas City Board of Trade. Table 1 on the next page summarizes that both wheat futures contracts have a combined $17.6 billion in open interest exposure (Panel A) and are also represented in the main commodity indices with an estimated $5.4 billion in total exposure (Panel B), as of the writing of this article.

Once a decision has been made to gain exposure to wheat futures contracts, possibly as part of a broad-based reflationary investment strategy, how should a fund manager analyze the two classes of wheat represented by CME Group futures contracts? This article will assist in answering this question, but first will provide some brief fundamental background on soft red winter wheat and on hard red winter wheat.

Background on Wheat Classes

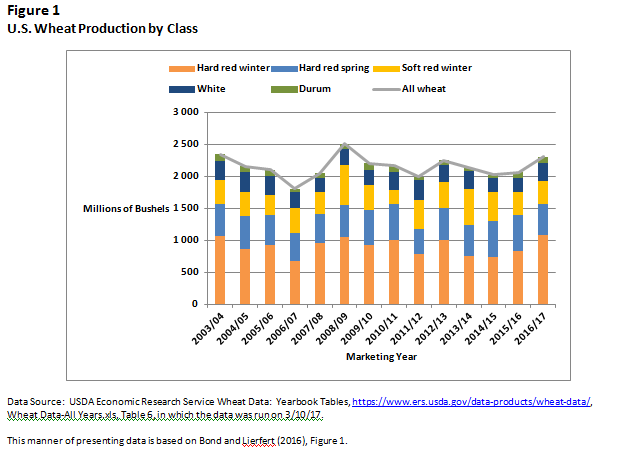

Types of wheat are classified according to three broad factors: (1) the timing of planting (encompassing winter or spring); (2) the level of protein (low, medium, or high); and (3) the color of the kernels (red or white). The more the protein, the “harder” the type of wheat is. Correspondingly, the less the protein, the “softer” the type of wheat is. Hard red winter (HRW) wheat “has excellent milling capabilities and baking characteristics … and is used in artisan and pan breads, Asian noodles, hard rolls, flat breads, and general purpose flour” while soft red winter (SRW) wheat is used in “pastries, cakes, cookies, crackers, pretzels, flat breads, and for blending flours,” as explained by the California Wheat Commission (2017). HRW wheat has tended to trade at a premium to SRW because of its higher protein content. As depicted in Figure 1, HRW wheat is by far the largest class of wheat produced in the U.S. According to estimates in Bond and Lierfert (2016), HRW wheat accounted for 45% of U.S. wheat production while SRW wheat accounted for just 16% of production.

The Two Wheat Futures Contracts: Liquidity and Spreading Opportunities

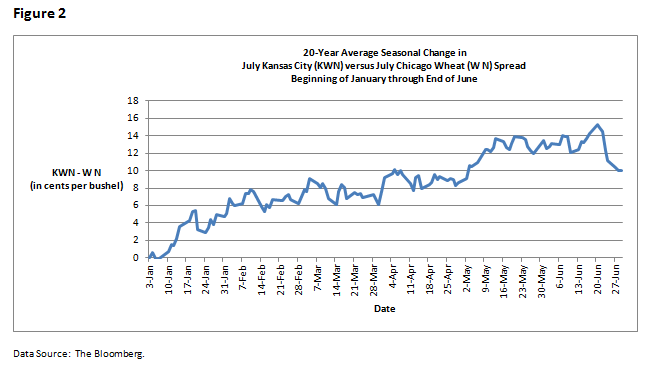

Despite the relative economic ordering of HRW and SRW wheat, the futures contract on SRW is where hedgers can obtain the greatest amount of liquidity provision from speculators. This can be ascertained both from Panel A of Table 1, showing the greater open interest and trading volume in the Chicago SRW contract versus the Kansas City HRW contract, and also from Panel C of Table 1, showing the greater amount of speculative spreading activity in the SRW contract. Futures contract liquidity providers typically manage risk by spreading so the amount of speculative spreading provides an indication of the level of speculative services that a commercial hedger may be able to access. One might expect that at least some commercial hedging in Kansas City HRW wheat futures contracts would have to be risk-managed by speculators using the Chicago SRW futures contract, given (a) the latter contract’s greater liquidity, and (b) how correlated the two contracts are, as shown in Panel D of Table 1. In this scenario, a commercial hedger would be entering into a short position in KC HRW futures contracts and a liquidity provider would correspondingly take the other side of this position by entering into a long KC HRW futures contract, and then hedge that position with a short Chicago SRW futures contract. But for this liquidity provision service to be consistently provided, there would likely have to be at least a slight statistical edge in the resulting speculative spread position (KC HRW futures – Chicago SRW futures) being a profitable trade over time. Winter wheat is usually harvested in the summer so one might expect hedging would be focused on the summer contracts. Figure 2 shows, as might be expected from the necessities of liquidity provision, that the July KC HRW futures contract has on average outperformed the July Chicago SRW futures contract over the past 20 years. What this long-term graph obscures is that the spread was only profitable twelve out of the last twenty years, but also that periodically the trade has had very large gains, giving a long-options-like payoff profile to this position. This latter feature is very attractive to investors and speculators alike and also helps in compounding returns. In fact, according to Bloomberg data, the futures-only returns from buying and rolling front-month KC HRW contracts has outperformed a similar strategy for Chicago SRW contracts by 4.0% per year from 2000 through 2016.

Fundamental Factors Impacting Wheat Spread Opportunities

What this initial analysis points to is that a fund manager should not automatically choose Chicago SRW wheat (W) futures contracts as the vehicle to express a bullish view on wheat. There has historically been a statistical edge in choosing Kansas City HRW wheat futures (KW) contracts. One might even term the spread strategy identified in Figure 2 as earning a type of risk premium where on average there is a return for liquidity provision by taking exposure in the less liquid contract relative to the more liquidly traded contract. But hedge fund managers and asset managers alike have higher expectations for trades and investments: an actively managed position must have superior (entry-and-exit) timing and risk-management rules and should not just passively involve entering into a spread trade with a statistical expectation of profit. Amongst the fundamental factors that can materially impact the KW – W spread from year-to-year include (1) whether SRW supply is particularly low; (2) whether HRW export demand is particularly low; and (3) the fluctuating protein content in HRW wheat. For example, regarding the first two points, Ehmke (2015) provided the following explanation for the steep premium of SRW to HRW, which occurred in November 2015: “Driving SRW’s rally against HRW is the serious shortage of quality SRW supplies … while HRW inventories are abundant because of its weak export pace,” quoting an official from U.S. Wheat Associates.

SRW Wheat Supply

The data sources for monitoring the three factors noted above include not only U.S. Department of Agriculture (USDA) reports, but also information from Commodity Futures Trading Commission (CFTC) data. The CFTC helpfully produces the weekly Disaggregated Commitments of Traders (DCOT) report, which provides a breakdown of commodity futures positions across the following four categories: (1) Producer/Merchant/Processor/User; (2) Swap Dealers; (3) Managed Money; and (4) Other Reportables. The first category provides a window into the amount of commercial hedging (and therefore, amount of supply that is being hedged for a commodity.) When SRW wheat supply is particularly low, one would expect two results: (1) the amount of producer hedging would be low, and (2) the KC HRW – Chicago SRW spread level would not be particularly large, as there would be upward pressure on SRW wheat prices. And indeed since June 13, 2006, the start of data in the DCOT report, when the Chicago wheat futures contract’s Producer/Merchant/Processor/User short-hedging participation has been one standard deviation below average, the KC HRW – Chicago SRW spread has been below average.

HRW Wheat Exports

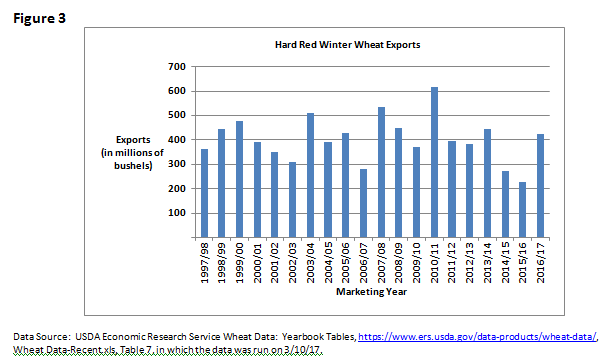

Regarding the relevant USDA data, Figure 3 draws from the USDA’s Economic Research Service in showing the history of HRW exports. The HRW exports in the 2014/2015 and 2015/2016 marketing years were one to two standard deviations below average since the 1997/1998 marketing year. In both of these years, the July KC HRW – July Chicago SRW spread did not appreciate as in the typical pattern shown in Figure 2.

Protein Content in Kansas Wheat

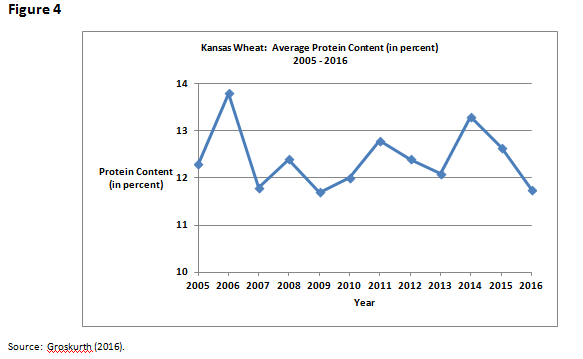

One can also refer to USDA reports for information on the fluctuating protein content of wheat grown in Kansas, as shown in Figure 4 on the next page. Ninety-five percent of wheat grown in Kansas is HRW, and 40% of U.S. HRW production is grown in Kansas. The above average protein-content showings in 2006, 2011, and 2014, depicted in Figure 4, correspond to times when the July KC HRW – July Chicago SRW spread did explosively well.

Conclusion

How should fund managers choose amongst wheat futures contracts if they are interested in expressing bullish economic and inflationary views through positions in the agricultural futures complex? They should consider the various factors that drive the relative performance of different classes of wheat futures contracts, as briefly covered in this article.

Endnotes

This article is based on Till (2017).

The author is grateful for research assistance from Hendrik Schwarz and Katherine Farren. That said, the views expressed in this article are the personal opinions of Hilary Till.

This article is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities or other financial instruments. The information contained in this article has been assembled from sources believed to be reliable, but is not guaranteed by its author. Any (inadvertent) errors and omissions are the responsibility of Ms. Till alone.

And finally, this article made liberal use of historical data and analyses in discussing past empirical relationships in the wheat futures markets. Consequently, the reader should be aware that the paper’s past results are obviously not guaranteed to continue into the future. The reader should be further aware that all commodity futures trading endeavors are, in practice, quite risky.

References

Bloomberg, 2016, “2017 Target Weights for the Bloomberg Commodity Index Announced,” Press Release, October 20.

Bond, J. and O. Liefert, 2016, “Wheat Outlook,” United States Department of Agriculture, Economic Research Service, September 14.

California Wheat Commission website, 2017, “U.S. and California Wheat Classes.” Accessed via website: http://www.californiawheat.org/industry/classes-of-us-wheat/ on April 9, 2017.

Ehmke, T., 2015, “Chicago’s SRW Wheat Trades at Rare Premium to Kansas City’s HRW,” Agweb.com website, November 17. Accessed via website: http://www.agweb.com/article/chicagos-srw-wheat-trades-at-rare-premium-to-kansas-citys-hrw-naa-tanner-ehmke/ on April 9, 2017.

Groskurth, D., 2016, “2016 Kansas Wheat Quality,” United States Department of Agriculture, National Agricultural Statistics Service News Release, September.

Keenan, M., 2017, “Commodity Special: 2017 Commodity Index Update FINAL UPDATE,” Societe Generale Cross Asset Research, Commodities, January 5.

S&P Global, 2016, “WTI Crude Oil Remains on Top as S&P Dow Jones Indices Announces 2017 Weights for the S&P GSCI,” Press Release, November 10.

Till, H., 2017, “Choosing Among the Wheat Futures Suite,” CME Group Report, May 16.

About EDHEC

Operating from campuses in Lille, Nice, Paris, London and Singapore, EDHEC is one of the world’s top 15 business schools. Fully international and directly connected to the business world, EDHEC commands a strong reputation for research excellence and the ability to train entrepreneurs and managers capable of breaking new ground. EDHEC functions as a genuine laboratory of ideas and produces innovative solutions valued by businesses. The School’s teaching is inspired by its research work and a focus on “learning by doing”, all with the aim of equipping people with the skills to succeed in business.