Fixed Income

Fixed-income investing is a strategic area of development for EDHEC-Risk Institute, with a number of increasingly relevant questions for institutional and individual investors, including efficient harvesting of interest rate and credit risk premia, the impact of a zero-interest rate environment on bond portfolio management, efficient interest rate risk management in retirement investing solutions an the relevance of a factor investing approach in fixed income markets.

This research programme is led by some of the world’s very best experts in the area of fixed-income securities, including Riccardo Rebonato – a leading expert in interest rate risk modelling and management, Frank J. Fabozzi – author and editor of over 100 reference textbooks in finance, and the manager of an eponymous series of authoritative finance books for practitioners and academics in numerous fields including fixed income analytics, financial modelling, mortgage-backed securities, municipal bonds, credit derivatives, and financial statement analysis, Dominic O’Kane – a specialist in credit modelling, derivative pricing and risk-management who was Head of Fixed Income Quantitative Research for nine years at Lehman Brothers, and Lionel Martellini – who has co-authored reference textbooks on fixed-income investment strategies.

EDHEC-Risk Institute has made recent efforts to provide a detailed, security-level analysis of the theoretical, statistical and practical challenges inherent in factor investing in sovereign bond markets, with a focus on factors that are relevant from a time-series perspective (factors such as the “level” or “slope” of the yield curve which for any maturity explain a large fraction of differences over time in bond returns) and on two factors responsible for many of the differences in the cross-section of bond returns, namely “value” and “momentum”, using economically justified proxies for these attributes.

Another research area we intend to explore in the coming years is whether economically significantly risk premia can be harvested in corporate bond markets, the two obvious potential sources of rewarded risk compensation being credit and liquidity. More research is needed in these directions, which are expected to become of strategic importance in fixed-income investing.

FUNDAMENTALS OF INSTITUTIONAL ASSET MANAGEMENT

by Frank J. Fabozzi, Francesco A Fabozzi

This book provides the fundamentals of asset management. It takes a practical perspective in describing asset management. Besides the theoretical aspects of investment management, it provides in-depth insights into the actual implementation issues associated with investment strategies. The 19 chapters combine theory and practice based on the experience of the authors in the asset management industry. The book starts off with describing the key activities involved in asset management and the various forms of risk in managing a portfolio. There is then coverage of the different asset classes (common stock, bonds, and alternative assets), collective investment vehicles, financial derivatives, common stock analysis and valuation, bond analytics, equity beta strategies (including smart beta), equity alpha strategies (including quantitative/systematic strategies), bond indexing and active bond portfolio strategies, and multi-asset strategies. The methods of using financial derivatives (equity derivatives, interest rate derivatives, and credit derivatives) in managing the risks of a portfolio are clearly explained and illustrated.

World Scientific - 2020

THE HANDBOOK OF FIXED INCOME SECURITIES, NINTH EDITION 9TH EDITION

by Frank Fabozzi (Author), Steven Mann (Author)

The definitive guide to fixed income securities―updated and revised with everything you need to succeed in today’s market.

One of the world’s leading experts on fixed income securities, Frank Fabozzi has gathered a peerless team of global experts who provide the newest and best techniques for winning in today’s markets. Fixed Income Securities, Ninth Edition is a matchless, one-stop resource for all your professional needs.

Several members of EDHEC-Risk Institute contributed to the book and co-authored the chapter on "Factor Investing in Sovereign Bond Markets":

Frank Fabozzi, PhD. CFA, CPA, Professor of Finance, EDHEC Business School

Jean-Michel Maeso, Senior Quantitative Researcher, EDHEC-Risk Institute

Lionel Martellini, PhD, Professor of Finance, EDHEC Business School and Director of EDHEC-Risk Institute

Riccardo Rebonato, PhD, Professor of Finance, EDHEC Business School, EDHEC-Risk Institute

This chapter describe the theoretical, empirical and implementation challenges related to factor investing in a single credit-risk-free issuer universe. In such a universe neither time-series nor cross-sectional differences in risk and performance can be explained by differences in creditworthiness, as they could be in the case of a multi-issuer universe. The key message is that it is possible to identify economically justifiable strategies that, after accounting for transaction costs and other forms of trading frictions, generate excess returns from investing in a relatively homogenous set of highly correlated securities. The profitability of these strategies can be due to a reward from factor exposure, systematic predictability resulting from market inefficiencies, behavioral biases, or a combination of the above.

McGraw Hill - 2020

BOND PRICING AND YIELD CURVE MODELING: A STRUCTURAL APPROACH

by Riccardo Rebonato

In this book, Riccardo Rebonato provides the theoretical foundations (no-arbitrage, convexity, expectations, risk premia) needed for the affine modeling of the government bond markets. He presents and critically discusses the wealth of empirical findings that have appeared in the literature of the last decade, and introduces the 'structural' models that are used by central banks, institutional investors, sovereign wealth funds, academics, and advanced practitioners to model the yield curve, to answer policy questions, to estimate the magnitude of the risk premium, to gauge market expectations, and to assess investment opportunities. Rebonato weaves precise theory with up-to-date empirical evidence to build, with the minimum mathematical sophistication required for the task, a critical understanding of what drives the government bond market.

Cambridge University Press - 2018

ADVANCED BOND PORTFOLIO MANAGEMENT: BEST PRACTICES IN MODELING AND STRATEGIES

by Frank J. Fabozzi, Lionel Martellini, Philippe Priaulet

In order to effectively employ portfolio strategies that can control interest rate risk and/or enhance returns, you must understand the forces that drive bond markets, as well as the valuation and risk management practices of these complex securities. In Advanced Bond Portfolio Management, Frank Fabozzi, Lionel Martellini, and Philippe Priaulet have brought together more than thirty experienced bond market professionals to help you do just that. Divided into six comprehensive parts, Advanced Bond Portfolio Management will guide you through the state-of-the-art techniques used in the analysis of bonds and bond portfolio management. Topics covered include: General background information on fixed-income markets and bond portfolio strategies The design of a strategy benchmark Various aspects of fixed-income modeling that will provide key ingredients in the implementation of an efficient portfolio and risk management process Interest rate risk and credit risk management Risk factors involved in the management of an international bond portfolio Filled with in-depth insight and expert advice, Advanced Bond Portfolio Management is a valuable resource for anyone involved or interested in this important industry.

Wiley - 2006

FIXED-INCOME SECURITIES: VALUATION, RISK MANAGEMENT AND PORTFOLIO STRATEGIES

by Lionel Martellini, Philippe Priaulet, Stéphane Priaulet

This is the first comprehensive textbook for students studying fixed-income securities, and is ideally suited to MBA, MSc and final year undergraduate students in Finance and related topics. The text offers an accessible and detailed account of interest rates and risk management in bond markets. It develops insights into different bond portfolio strategies, and illustrates how various types of derivative securities can be used to shift the risks associated with investing in fixed-income securities. It also provides extensive coverage on all sectors of the bond market, and the techniques for valuing bonds. In addition, explanation is given of state-of-the-art techniques for bond portfolio management, including: A description of numerous fixed-income assets and related securities, namely zero coupon government bonds, coupon bearing government bonds, corporate bonds, exchange-traded bond options, bonds with embedded options, floating rate notes, caps, floors and collars, swaptions, credit derivatives, mortgage-backed securities, etc.The development of tools to analyse interest rate sensitivity and to value fixed- income securities, with an emphasis on active and passive bond management, and an overview of techniques used by mutual fund and also hedge fund managers. With numerous worked examples covering the valuation, risk management and portfolio strategies of fixed income securities, and imaginative discussion of important topics such as deriving the zero yield curve, deriving credit spreads, and hedging interest rate risk, the text provides an accessible route into the complex worlds of fixed income securities.

John Wiley & Sons - 2003

MODERN PRICING OF INTEREST-RATE DERIVATIVES: THE LIBOR MARKET MODEL AND BEYOND

by Riccardo Rebonato

n recent years, interest-rate modeling has developed rapidly in terms of both practice and theory. The academic and practitioners' communities, however, have not always communicated as productively as would have been desirable. As a result, their research programs have often developed with little constructive interference. In this book, Riccardo Rebonato draws on his academic and professional experience, straddling both sides of the divide to bring together and build on what theory and trading have to offer. Rebonato begins by presenting the conceptual foundations for the application of the LIBOR market model to the pricing of interest-rate derivatives. Next he treats in great detail the calibration of this model to market prices, asking how possible and advisable it is to enforce a simultaneous fitting to several market observables. He does so with an eye not only to mathematical feasibility but also to financial justification, while devoting special scrutiny to the implications of market incompleteness. Much of the book concerns an original extension of the LIBOR market model, devised to account for implied volatility smiles. This is done by introducing a stochastic-volatility, displaced-diffusion version of the model. The emphasis again is on the financial justification and on the computational feasibility of the proposed solution to the smile problem. This book is must reading for quantitative researchers in financial houses, sophisticated practitioners in the derivatives area, and students of finance.

Princeton University Press - 2002

FIXED-INCOME SECURITIES: DYNAMIC METHODS FOR INTEREST RATE RISK PRICING AND HEDGING

by Lionel Martellini, Philippe Priaulet

This book provides a thorough explanation of modern methods for pricing and hedging fixed-income securities (i.e. government bonds, corporate bonds, treasury bills, and interest rate derivatives, etc.). The pricing and hedging of fixed-income products is technically more complicated than the pricing and hedging of equity instruments. The interest rate variable, which needs to be modeled, is not a traded quantity and this makes it very difficult to price and hedge the security. In this book, the authors set out to explain the various modeling techniques that can be used to price the various securities. Structured in a very accessible fashion, the first part of the book is devoted to hedging and pricing certain cash flows and the second part of the book then focuses on pricing and hedging uncertain cash flows, such as cash flows from derivatives.

John Wiley & Sons - 2001

Description

EDHEC is launching the EDHEC Bond Risk Premium Monitor in September 2017. Its purpose is to offer to the investment and academic communities a tool to quantify and analyse the risk premium associated with Government bonds (with an initial focus on US Treasuries).

We calculate the risk premium using two distinct methods: (i) a purely statistical method and (ii) a model-based method.

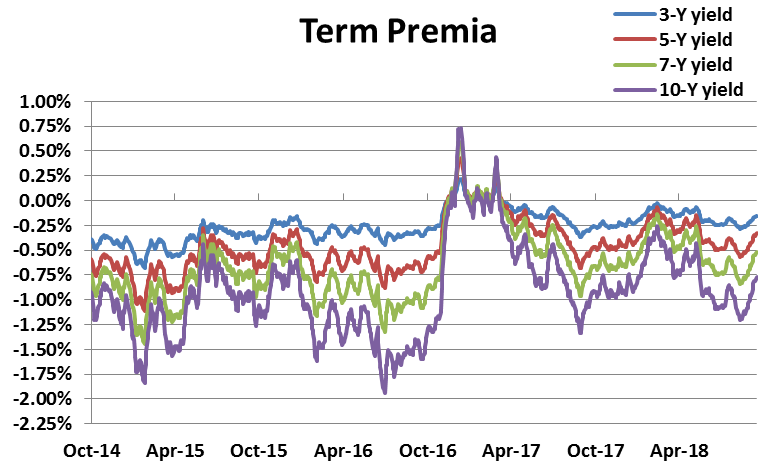

Term Premia Estimates - Highlights January 2020 / May 2020

The Ever-Falling Rate Expectations

The Fed began producing its ‘dot plot’ (otherwise known as ‘the blue dots’) in January 2012 to give clear guidance to the market of where the members of the Monetary Committee saw the more likely value for the Fed funds at different horizons in the future.

For short horizons, it is not too surprising that these projections may change, as information about the speed of the recovery, inflationary pressures, unemployment and other macrofinancial variables is progressively revised.

The ‘last blue dot’ should be different. This last point represents the projection over the ‘very long run’ of the most likely level for the Fed Funds – as made by the very people in charge to set the rate! Barring truly secular in nature, this quantity should be very stable, as it reflects a combination of expectations about long-term inflationary pressures and real growth in the economy.

In reality, as Fig 1 shows, it has been anything but. When the Fed began communicating its monetary intentions via the dot plot (as recently as January 2012, ie, almost exactly 8 years ago), it expected the Fed funds in the distant future to be as high as 4.12%. At the last Committee meeting, the same long-term expectation of the Fed funds was 2.54%: more than 150 basis points lower.

At every single meeting, the expectation has either remained unchanged, or has drifted lower. It has done so by changing (always downwards) far more than the dispersion of opinions (which has a very stable standard deviation of about 30 basis points) would justify. What has been happening?

Make no mistake: when monetary economists predict a future nominal ‘short rate’ as low as 2.50%, they must either believe that the Fed will not be able to prevent a collapse in inflation (which can only be associated with difficult economic conditions); or that the real rate of growth will be extremely low; or both. A far cry from what the equity valuations seem to imply at the moment. Either the economists or the S&P500 must be wrong.

With such a dramatic fall in expectations, one could be forgiven for expecting that risk premia should have widened. After all, the nominal yield that we see should be the sum of expectations (that have fallen) and risk premia. Hardly so. The 10-year nominal yield, as of this writing, is around 160 basis points. Suppose that the expected inflation is 2.00% (below the official target), and that there is no compensation for inflation risk. The sum of the real rate and the real-rate risk premium is therefore around minus 50 basis points. Even a rather gloomy projection for 10-year real growth of 1% forces the risk premium to be a negative -150 basis points. How can this make sense?

The only way to rationalize this extremely low value is to remember that a positive risk premium is compensation for being paid well in good states of the world, and poorly when you would need the money. Conversely, a negative risk premium attaches to assets that pay well when you feel poor, and vice versa. As we move beyond 10 years of almost uninterrupted rise in the equity market, the value of the ‘Greenspan (now Powell) put’ is becoming more and more keenly felt. If you add in the complications of an election year, and a US President who is happy to lean on the Chairman of the Fed as robustly as few Presidents have done in recent memory, and it is easy to see that the market is betting the farm on the Fed cavalry coming to the rescue at the next serious bump in the road.

If looked at in this light, the 150 basis points of negative risk compensation are the risk premium investors seem to be willing to pay to offset their equity risk. For this to be a ‘good insurance price’, the Treasury hedge has to work close to perfection. The room for error that current yield levels leave is extremely thin.

FAQs

EDHEC is launching the EDHEC Bond Risk Premium Monitor in September 2017. Its purpose is to offer to the investment and academic community a tool to quantify and analyse the risk premium associated with Government bonds (with an initial focus on US Treasuries).

The following FAQs provide detailed explanations of what it can offer.

The EDHEC Bond Risk Premium Monitor is a suite of tools that can be used to estimate the risk premium embedded in US Treasury bonds of different maturities.

In general, the risk premium can be thought of as the compensation investors require in order to bear the risks entailed in holding an asset. More precisely, it is proportional to the covariance between the pay-off of a security and the consumption of the investor. If we proxy consumption with return on investments, the risk premium should be proportional to the covariance between the pay-off of a security and the return from a broad market index (for example, the S&P 500).

For a precise definition, see Cochrane (2001), Asset Pricing, Princeton University Press, or Rebonato (2018), Bond Pricing and Yield Curve Modelling – A Structural Approach, Cambridge University Press, Chapter 15.

In the case of (riskless) bonds, the risk premium is associated with the strategy of being ‘long duration’, (i.e. of funding a long position in a long-maturity bond by shorting a short-maturity bond). The strategy is often referred to as a ‘carry’ trade.

A high risk premium suggests that, on average, one can expect to make money from investing in long-term bonds and funding at the short end. From an asset manager’s perspective, a high risk premium suggests that it is a good time to be ‘long duration’ with respect to the chosen bond benchmark.

Risk premia provide timing (rather than cross-sectional) investment information. They answer the question, “Is today a good (bad) time to be long duration?” They do not answer the question, “Given that I have to be invested today, which bond gives the most attractive expected return?”

Risk premia also allow the market expectations about the future path of the short rate (Fed funds) to be extracted from the market yields.

From an asset pricing perspective, if an asset ‘hedges’ the risk from the market portfolio, then it will command a negative risk premium (we pay for fire insurance above the actuarial odds). So, if bonds hedge equity risk very effectively (the Greenspan/Bernanke/Yellen ‘put’), investors may then be willing to accept negative risk compensation for their hedging properties. Less precisely, it is often argued that, in an environment of extremely low (real) returns, ‘hunger for yields’ can drive risk premia into negative territory.

There is ample evidence that the risk premium is not a constant, but rather that it depends on the state of the economy. In turn, some aspects of the state of the economy are reflected in the shape the yield curve – so, the magnitude and sign of the risk premium depends (in part) on the shape of the yield curve.

We calculate the risk premium using two distinct methods: (i) a purely statistical method and (ii) a model-based method.

The statistical estimate of the risk premium is based on the analysis of the returns made by investing in a long-maturity bond and funding the position at the short end of the yield curve (the ‘carry’ strategy). If forward rates were unbiased expectations of future rates, then, on average, the carry strategy would make no money. Once a time series of excess returns has been obtained, that time series can be regressed against a number of candidate return-predicting factors, and it can be determined whether any of these factors are statistically significant. It must be stressed that, in order to avoid data mining and ‘factor fishing’, it is very important to give an economic explanation for the return-predicting factor.

Different return predicting factors give similar, but not identical, estimates of the risk premia. The more complex the return-predicting factor, the better the in-sample fit, but the grater the danger of over-fitting (and therefore of poor out-of-sample-prediction). We present the predictions from a (small) number of return-predicting factors, and the average of the predictions.

We stress that changes in risk premia are more reliably estimated than the level of risk premia (the ‘slopes’ of the regressions have tighter confidence bands than the ‘intercepts’).

The return-predicting factors were chosen on the basis of robustness (out-of-sample performance) and predictive power. We mainly focus on four factors:

- the Cochrane-Piazzesi (2005) ‘tent-shaped’ factor (III) ;

- the Cieslak-Povala (2010a, 2010b) cycle-based factor (IV) ;

- the ‘restricted’ Cieslak-Povala factor (V);

- the unconditional slope and the level cycle (VI).

We also present the average of the four predictions, which is arguably the most reliable estimator.

Statistical models implicitly assume that the future looks like the past. As, over the last few years, authorities have been engaged in unprecedented monetary operations (QE, negative interest rates, etc.), past regularities may not apply to the present market conditions. Purely statistical models can therefore be ‘tricked’ by spurious similarities with past yield curve configurations. This is where a model can help, by adding financial information to the purely statistical data.

The extra financial information comes from the so-called ‘blue dots’ – predictions by members of the Monetary Policy Committee of the U.S. Fed about the future path of the fed funds rate. So, with the statistical approach, we try to directly estimate the risk premium, and we obtain the expectations as a by-product. With the model-based approach, we try to estimate the expectations and we obtain the risk premia. (In both cases, we take the market yields as given.

The model used belongs to the class of affine models. It is unique, however, in that it allows the market price of risk to be stochastic: instead of being a deterministic function of the shape of the yield curve, it is still only correlated with the established return-predicting factors. This means that, given a particular shape of the yield curve, the market price of risk does not always have to assume the same value. This is particularly important given the atypical monetary conditions encountered in the last ten years or so.

(I) Strictly speaking, one should also take convexity into account. For a discussion, please refer to Rebonato (2018). Bond Pricing and Yield-Curve Modelling – A Structural Approach, Cambridge University Press, Chapters 20-21.

(II) See Rebonato (2018). Bond Pricing and Yield-Curve Modelling – A Structural Approach, Cambridge University Press, Chapter 24.

(III) See Cochrane, J. H. and M. Piazzesi (2005). Bond Risk Premia. American Economic Review 95(1): 138-160; for technical details, and the regression coefficients, see https://www.aeaweb.org/aer/data/mar05_app_cochrane.pdf (accessed on 25 November 2014).

(IV) Cieslak, A. and P. Povala (2010a). Understanding Bond Risk Premia. Working paper – Kellogg School of Management and University of Lugano, available at

https://www.gsb.stanford.edu/sites/default/files/documents/fin_01_11_Cie..., accessed on 5 May 2015, and Cieslak, A. and P. Povala (2010b). Expected Returns in Treasury Bonds, working paper, Northwestern University and Birbeck College, forthcoming in Review of Financial Studies.

(V) ibid

(VI) Hatano, T. (2016). Investigation of Cyclical and Unconditional Excess Return Predicting Factors. MSc thesis – Oxford University.

(VII) See Rebonato (2018). Bond Pricing and Yield-Curve Modelling – A Structural Approach, Cambridge University Press, Chapter 25 for a discussion of this point.

(VIII) For a chapter-length description of affine models, see, Piazzesi M. (2010), Affine Term Structure Models, Chapter 12 in Handbook of Financial Econometrics, Elsevier, or Bolder, D. J. (2001). Affine Term-Structure Models: Theory and Implementation, Bank of Canada, Working paper 2001-15, available at http://www.bankofcanada.ca/wp-content/uploads/2010/02/wp01-15a.pdf , accessed on 11 August 2017. For a book-length treatment, see Rebonato (2018), Bond Pricing and Yield-Curve Modelling – A Structural Approach, Cambridge University Press.

(IX) For a detailed description of the model, see Rebonato (2017). Reduced-Form Affine Models with Stochastic Market Price of Risk, International Journal of Theoretical and Applied Finance(forthcoming).

Publications

International Journal of Theoretical and Applied Finance

AFFINE MODELS WITH STOCHASTIC MARKET PRICE OF RISK

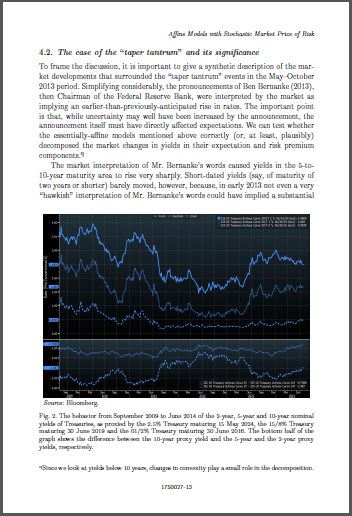

In this paper we discuss the common shortcomings of a large class of essentially-affine models in the current monetary environment of repressed rates, and we present a class of reduced-form stochastic-market-risk affine models that can overcome these problems. In

particular, we look at the extension of a popular doubly-mean-reverting Vasicek model, but the idea can be applied to all essentially-affine models.

Read more »

18 May 2017

Related articles

Fed's low confidence signals recession, Investors Chronicle, 17 January 2019

Is the yield curve telling us that a recession is around the corner?, EDHEC Vox, 10 January 2019

Why Is the Market Not Believing the Fed?, EDHEC-Risk, 12 April2019

- "Defining and exploiting value in US Treasury bonds” - ETF Stream (18/06/2020)

- "Why a top quant wants to be wrong about markets" - Risk.Net (24/05/2020)

- "Buzz around factor investing in fixed income is growing” - Financial Times (23/09/2019)

- Smart Beta Bond ETFs May Be Beginning to Attract Attention - ETF Trends (23/09/2019)

- "A promising start, but more work is needed" - ETF Stream (01/09/2019)

- "EDHEC’s Rebonato predicts ‘new dawn’ in fixed income investing” - ETF Stream (22/08/2019)

- "The (Many) Problems of an Inverted Yield Curve” - Traders Magazine (17/09/2019)

The research programme currently benefits from the support of PIMCO in the context of a research chair on fixed-income term structure modelling and volatility and on time-series and cross-sectional results of bond risk premia.

The research programme currently benefits from the support of PIMCO in the context of a research chair on fixed-income term structure modelling and volatility and on time-series and cross-sectional results of bond risk premia.

It has also benefited from the support Amundi for a research chair on ETF, Index and Smart Beta Investment Strategies, and that of Banque de France Gestion for a research chair on the benefits of scientific and naive diversification for sovereign and corporate bond portfolios.

About EDHEC

Operating from campuses in Lille, Nice, Paris, London and Singapore, EDHEC is one of the world’s top 15 business schools. Fully international and directly connected to the business world, EDHEC commands a strong reputation for research excellence and the ability to train entrepreneurs and managers capable of breaking new ground. EDHEC functions as a genuine laboratory of ideas and produces innovative solutions valued by businesses. The School’s teaching is inspired by its research work and a focus on “learning by doing”, all with the aim of equipping people with the skills to succeed in business.